Contractual risk management: risk mitigation and insurer response

Gallagher’s conference workshop explained exactly what is and isn’t covered by an insurance policy. In this article, Nick Wilson and Mark Rubidge explain the key points for achieving a watertight contract.

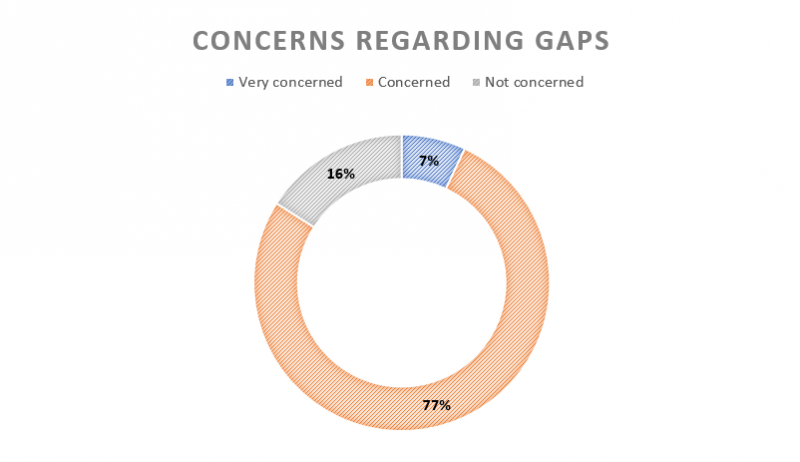

In a survey of Airmic members registered to attend our conference workshop, 84% of respondents said that they were either concerned or very concerned regarding gaps which may exist between their contractual responsibilities and the coverage provided by their insurance policies.

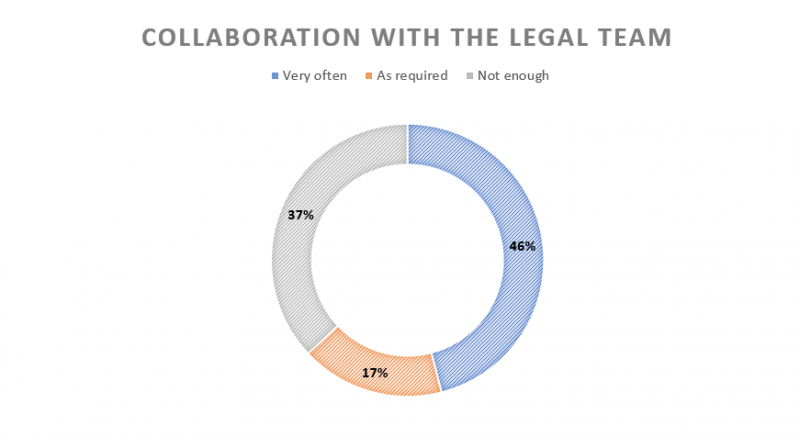

As part of the same survey, 37% of members also commented that they did not collaborate with their legal teams enough to ensure a joined-up risk management approach to contract terms.

Within this article we explore the consequences of uninsured loss and what insureds can do to improve their risk management strategy.

Consequences of uninsured loss

It is important to remember that your contracts bind you, they do not bind your insurers. Therefore there is no guarantee that your insurers will indemnify you in respect of any claims. If insurers will not provide an indemnity:

- You are still liable to perform your contract;

- You may have to pay any sums due under the contract in respect of any losses occasioned by breach;

- You will need to factor in the defence costs of instructing your own lawyers to defend the claim;

- Consequences are potentially severe and could lead to financial hardship, even insolvency, if the claim is substantial enough;

- There is the possibility of personal liability on directors depending on the terms of the contract.

Insurance cover response

No insurance policy will cover every eventuality arising under a contract and as such there may be areas of exposure for which you are not covered. Liability policies (public liability, product liability, cyber liability, professional indemnity) will generally require the existence of a legal liability. This is in contrast to many standard indemnity clauses found within contracts which:

- Impose liability in respect of “all losses, claims, damages, expenses and costs” that are caused by (or linked to) a particular breach of contract or duty;

- Are onerous, as they operate regardless of any legal liability, mitigation or reasonable foreseeability;

- Go far beyond common law.

Therefore it is essential that cover is specifically negotiated for contractual liabilities that are accepted by the business. As part of this process:

- Fully disclose the whole contractual matrix to brokers / insurers to review and advise on what can be covered under the insurance policy;

- Identify insured vs uninsured areas to ensure the business is fully aware of the self-insured risks that are being accepted under contract;

- Where appropriate, consider the use of collateral warranties to create the legal relationship between the buyer and any sub-contractors / suppliers that do not have a direct legal relationship with the buyer.

Conclusion

Having a good risk management strategy is crucial. This involves:

- A good connection between legal/risk departments and the business, collaborating at the contract drafting stage of negotiations;

- Knowing which clauses are being used and whether they are/are not insured;

- Seeking specific extensions where required;

- Looking to fill gaps where matters are not insured (e.g. by contractual means);

- Maintaining a good audit process to manage the time lag between projects and claims, particularly where policies are “claims made”.

This article is based on a workshop presented at Airmic’s annual conference in Harrogate.

Nick Wilson, risk manager, Gallagher

Mark Rubidge, director, Gallagher